Why financial planners say to stop chasing a magic number

«It’s hard to save for a future that feels abstract when the present feels urgent,» said Douglas Boneparth, a certified financial planner and president and founder of Bone Fide Wealth in New York, and a member of the CNBC Financial Advisor Council. Rising costs and credit card debt, he stressed, are not excuses — they are the reality people are navigating.

Rather than fixating on a single savings target, Boneparth recommends building consistent habits. Someone who saves regularly, works to reduce high-interest debt, and invests early «can close more ground than they think,» he said — even if their current balance sits at $12,000 while the goal is $1.2 million.

The right retirement number is also deeply personal. It depends on where someone lives, their lifestyle, and when they plan to stop working. «You may need more or significantly less,» Boneparth said. «It depends.» A blanket figure, while useful as a benchmark, cannot substitute for an individual assessment with a qualified financial advisor.

Billions in retirement funds sitting idle in cash

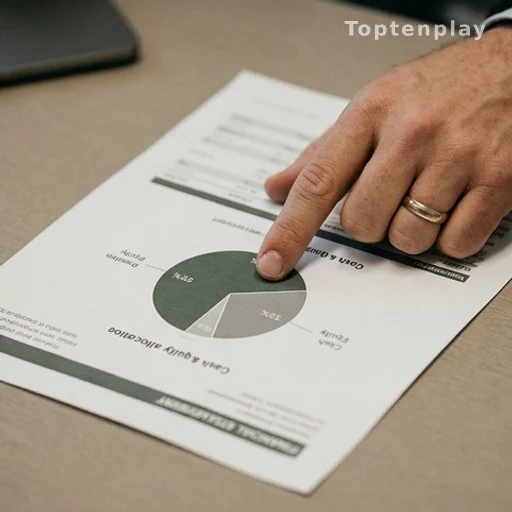

Beyond the savings gap, Schroders identified a separate problem in how existing retirement funds are allocated. 24% of retirement plan participants said they do not know how their savings are invested — a significant share of people with no visibility into their own financial future.

Among those who do know, the breakdown is striking: 26% of retirement savings are held in cash, nearly matching the 27% allocated to equities. For long-term investors, that balance carries real costs. «For participants with long-term horizons, excessive cash can lead to a meaningful opportunity cost,» Boyden said.

The motivations behind those cash holdings are understandable: 53% cited the pursuit of safety, 44% said they wanted to diversify, and 33% said they were waiting for the right moment to invest. For those unsure of their next step, Boneparth offered a direct recommendation: «Most people who feel stuck haven’t sat down with someone to map it out. That conversation alone tends to shift things.»

Suggested Posts

AI financial advice: biased, inconsistent and sometimes just wrong

Artificial intelligence tools give personal finance advice that can be inaccurate, inconsistent and demographically biased — and the results vary significantly depending on which…